What You Ought to Know:

– In response to the inaugural State of AI in Healthcare Report from Menlo Ventures, AI spending within the sector is surging, reaching $1.4 billion in 2025—almost tripling final 12 months’s complete. Remarkably, healthcare organizations are actually adopting AI options 2.2x quicker than the broader economic system, shortly shedding its popularity as a know-how laggard.

– The report, based mostly on a survey of over 700 healthcare executives, signifies that the business is quickly deploying specialised, domain-specific AI instruments to deal with crucial points like administrative overhead, doctor burnout, and R&D inefficiency. The proof reveals that for a lot of organizations, the query is now not if AI is effective, however how briskly it may be deployed to the manufacturing atmosphere.

Key Findings: The Shift from Pilot to Manufacturing

The info confirms that healthcare is at an inflection level, with high-velocity adoption and spending concentrated in quick ROI areas.

- Spending Explodes: Complete AI spending in healthcare is as much as $1.4 billion in 2025, marking nearly a three-fold enhance from the prior 12 months. This fast funding has been environment friendly, with the overwhelming majority of the cash flowing into manufacturing deployments, not simply proof-of-concept pilots.

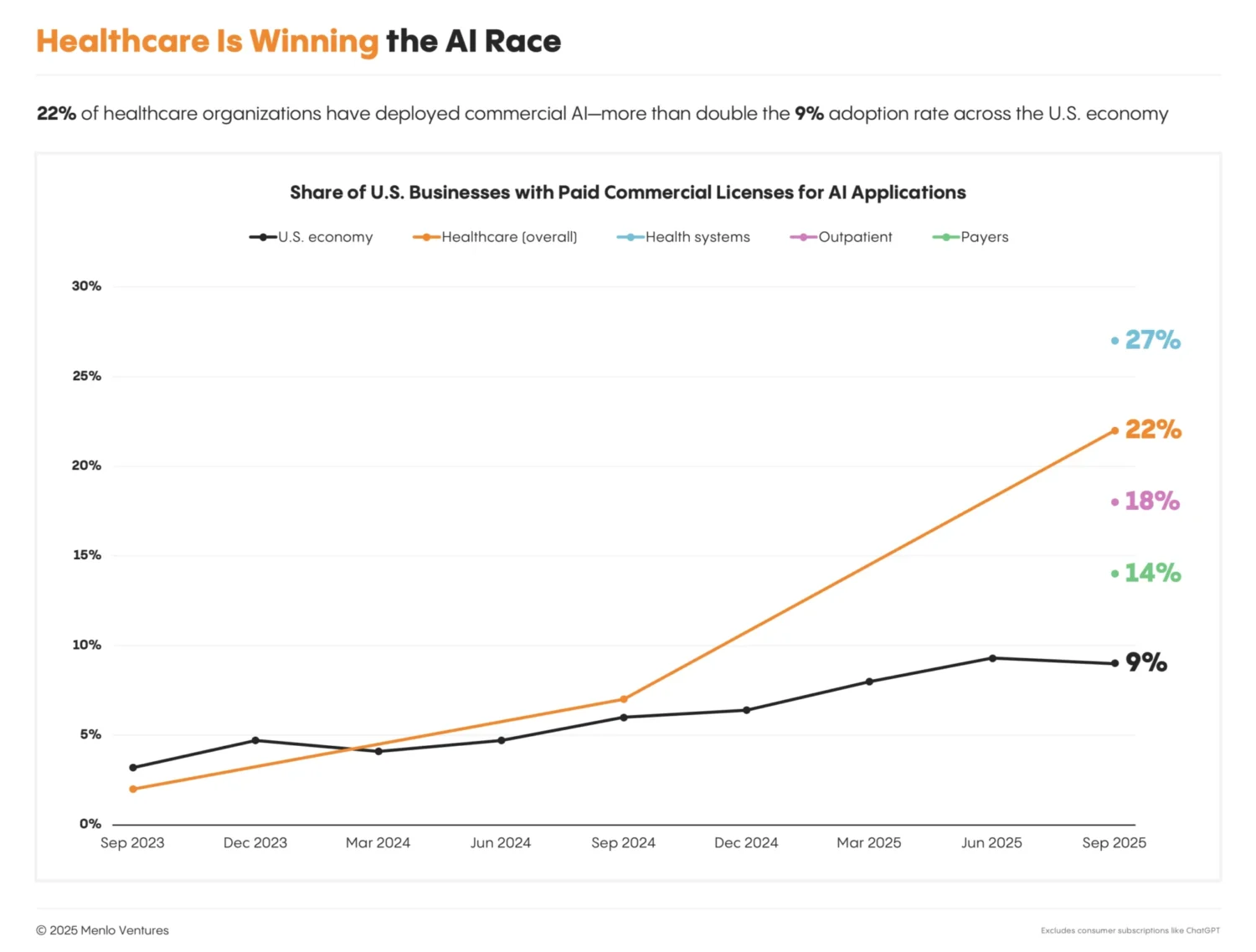

- Adoption Management: Healthcare has flipped the script, now adopting AI 2.2x quicker than the broader economic system. 22% of healthcare organizations have deployed domain-specific AI options, a large 7x enhance over 2024. Well being programs are main the cost at 27% adoption, outpacing outpatient suppliers (18%) and payers (14%).

- Unicorn Manufacturing facility: The surge in exercise has produced eight AI unicorns throughout key areas like medical documentation, RCM, and payer operations—greater than some other vertical AI class.

The place the {Dollars} Are Flowing: Administrative Aid

The market’s largest breakout classes are people who provide quick aid to the monetary and human prices of administrative work.

- Supplier Dominance: Of the $1.4 billion flowing into the market, suppliers account for $1 billion (75%) of the spend, highlighting their pressing want to enhance effectivity and fight employees shortages.

- The Large Two: Two classes dominate spending: ambient scientific documentation ($600 million), which targets doctor burnout by automating note-taking, and coding and billing automation ($450M), which helps recuperate income misplaced to errors.

- Quickest-Rising Alternatives: AI is aggressively transferring into different administrative service gaps. Affected person engagement options are rising at +20x year-over-year, and AI for prior authorization is accelerating at +10x year-over-year. These classes, which contain automating workflows that have been historically guide and staff-intensive, are turning companies {dollars} into software program {dollars} for the primary time.

The Procurement Divide and Market Tensions

The tempo of know-how adoption differs considerably throughout the sector, and the rise of AI is creating friction between revolutionary startups and entrenched incumbents.

Suppliers Speed up, Payers Deliberate

Whereas suppliers are racing to seize operational advantages, payers are exercising higher warning. Well being programs have dramatically shortened their shopping for cycles by 18%, and outpatient suppliers by 22%, as they transfer shortly to deploy manufacturing programs.

In distinction, payers have seen their shopping for cycles lengthen by 20%, indicating that they continue to be in a extra cautious, deliberative, and experimentation part. Payers’ main concern is that supplier AI instruments, by optimizing billing and dashing up submissions, will result in a surge in claims quantity and doubtlessly enhance medical prices.

The Startup vs. Incumbent Showdown

Startups at present seize 85% of all generative AI spend in healthcare. They dominate with AI-native structure in breakout fields like ambient scribing and chart evaluate. Nevertheless, the incumbents are preventing again fiercely. The marketplace for ambient scribes—AI’s first breakout class—is going through a retention disaster, with 67% of outpatient suppliers anticipating to modify distributors inside three years, viewing the know-how as more and more commoditized.

The info reveals a crucial stress: though startups are profitable the income battle now, most prospects nonetheless report a slight choice for getting AI from their incumbent EHR supplier (Epic, Oracle Well being, and so on.) for essential features like coding, billing, and scientific choice help. The deep integration and trusted relationship of the incumbent stay a strong, enduring benefit.

Life Sciences: Constructing Proprietary Defenses

The pharma and biotech sector is approaching AI with a unique technique, targeted much less on shopping for off-the-shelf software program and extra on constructing inside IP.

- Proprietary Fashions: 66% of pharma and biotech firms are prioritizing the trouble to construct or fine-tune proprietary fashions tailor-made for biology and drug discovery.

- R&D Focus: Their predominant space of curiosity is R&D information evaluation (63%), leveraging AI to ingest public information, analyze experimental outcomes, and speed up the pricey, time-consuming drug growth lifecycle.

Healthcare Automation: The Most Important Alternative

The report concludes that essentially the most vital alternative lies forward: automating the $740 billion in complete annual U.S. administrative spending that was beforehand inaccessible to software program. The subsequent wave of innovation shall be outlined by firms that may resolve the “product and workflow issues” of integrating these highly effective AI instruments into the messy, complicated actuality of affected person care.

Click on here to study extra in regards to the State of AI in Healthcare Report.

{kind=link}