What You Ought to Know

- The Actuality Test: In HGP’s 20-year retrospective, the decision is harsh: expertise delivered on workflows however failed on economics. Since HGP’s founding, U.S. healthcare spending has doubled to $5.3 trillion, proving that digitization alone doesn’t equal effectivity.

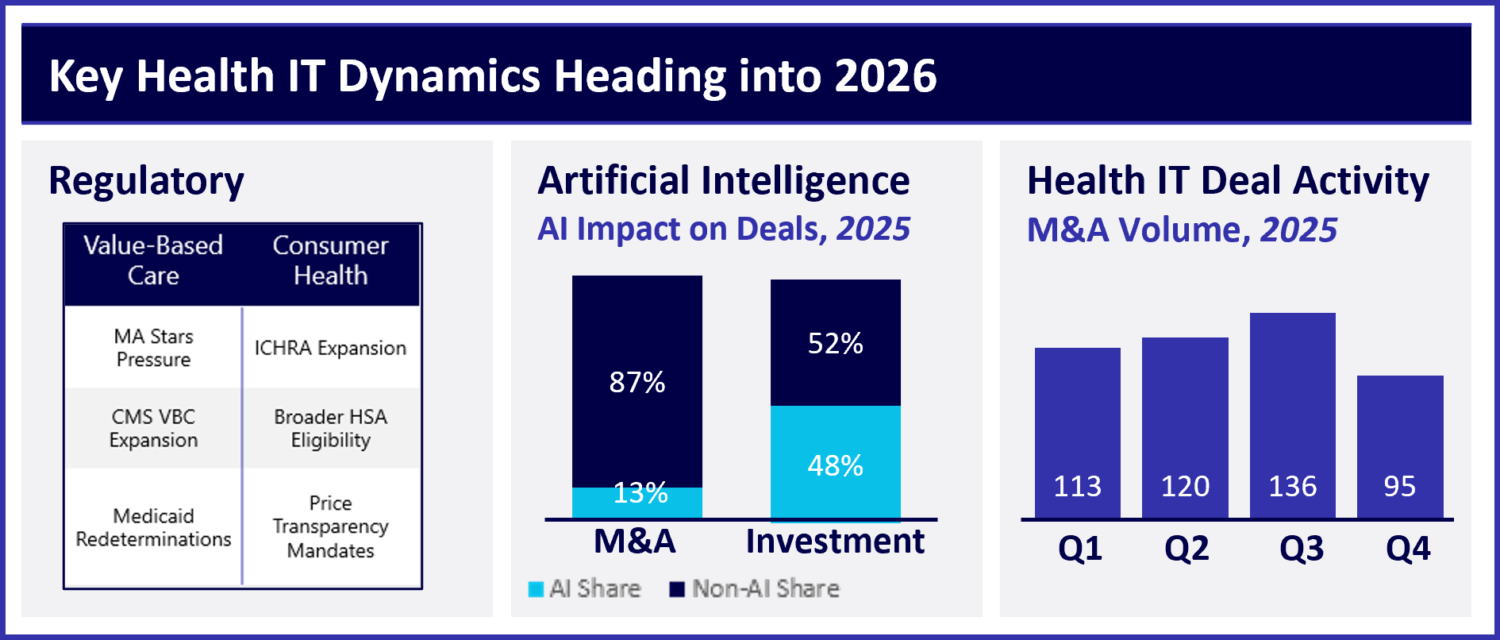

- The Market Rebound: Regardless of the cynicism, the deal market is roaring again. Q3 2025 noticed a document 136 M&A offers, and valuations have settled comfortably above pre-pandemic ranges (approx. 5.1x income), signaling that the “Nice Reset” is over.

- The AI Divide: An enormous hole exists between hype and exit. Whereas 50% of funding capital went to AI-native corporations in 2025, solely 13% of M&A offers concerned them. Strategic patrons are buying elementary workflow corporations, not simply algorithms.

HGP 2026 Market Evaluation: M&A Hits File Highs as AI Funding Captures 50% of Capital

In response to the January 2026 Market Review from Healthcare Growth Partners (HGP), the business has achieved “near-universal” adoption of expertise, but the financial returns stay elusive. Since HGP’s founding twenty years in the past, U.S. healthcare spending has practically doubled, rising from $2.5 trillion to $5.3 trillion.

“Well being IT has meaningfully modernized workflows and knowledge seize,” the report notes, “whereas its influence on outcomes and its financial worth has been restricted.”

Nevertheless, as we enter 2026, the report suggests the business isn’t collapsing—it’s maturing. With inflation moderating to 2.6% and rates of interest easing, the market is shifting from “regulatory compliance” to “financial accountability.”

The “Add-On” Period of AI

Maybe probably the most counter-intuitive discovering for 2026 is the position of Synthetic Intelligence. The prevailing narrative is that AI startups will disrupt legacy incumbents (like Epic or Oracle). HGP’s knowledge suggests the alternative: Incumbents are consuming the innovation.

“To this point, AI is proving additive, not existential, for incumbents,” the analysts write.

The numbers reveal a bifurcated market:

- The Hype: Buyers are pouring cash into the dream. In 2025, 50% of US Well being IT funding {dollars} flowed to AI-native corporations.

- The Actuality: Patrons are buying utility. Solely 13% of M&A and buyout transactions concerned corporations closely advertising and marketing AI capabilities.

Strategic acquirers are prioritizing “income sturdiness” and “embedded workflows” over generative magic. They’re shopping for the monitor, not the prepare.

The Regulatory Fork within the Street

The report identifies a essential divergence in how the federal government is shaping the market. Regulation is splitting healthcare into two distinct financial fashions:

- Institutional Worth-Primarily based Care: CMS is doubling down on long-term accountability (e.g., the brand new ACCESS mannequin for persistent care). This favors platforms with deep knowledge moats and capital capability.

- Client-Directed Well being: Concurrently, affordability pressures are pushing markets towards transactional dynamics (ICHRAs, HSAs, Worth Transparency). This favors instruments constructed for pace, entry, and retail-like effectivity.

Firms straddling these two worlds could discover themselves pulled aside. “The result’s two parallel funding theses,” HGP notes.

M&A: The Wholesome “New Regular”

After the “COVID sugar excessive” of 2021 and the next crash, 2025 marked the return of a wholesome center class in deal-making. Quarterly M&A quantity hit an all-time excessive in Q3 2025 with 136 offers. Valuations for software program corporations have stabilized at 5.1x income—decrease than the COVID peak of 8.1x, however notably larger than the pre-pandemic common of 4.6x.

Nevertheless, getting these offers accomplished requires creativity. The report highlights an increase in “versatile deal constructions,” with patrons utilizing earnouts and rollover fairness to bridge the hole between purchaser warning and vendor optimism.

The Verdict

2026 feels totally different not as a result of the issues are solved, however as a result of the business has stopped pretending that software program solves all the things.

As HGP concludes, the subsequent decade received’t be formed by “regulatory incentives” (like Significant Use), however by “accountability and economics.” The winners received’t be those who digitize the chart; they would be the ones who lastly—after twenty years—determine how you can decrease the invoice.

{kind=link}