What You Ought to Know:

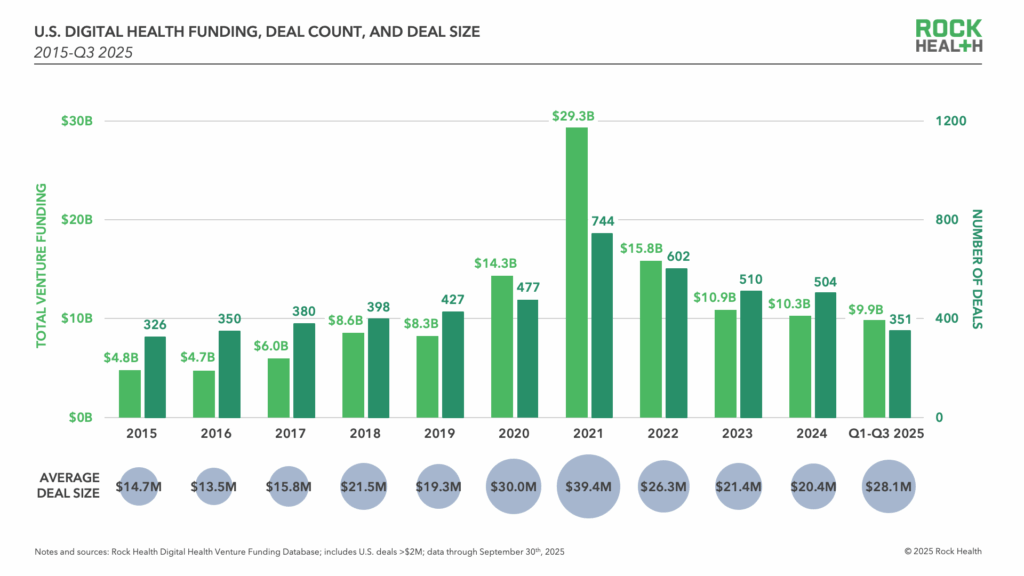

– The U.S. digital health sector noticed $3.5B in enterprise funding throughout 107 offers in Q3 2025, contributing to a year-to-date whole of $9.9B, based on Rock Health’s Q3 2025 report. Whereas this tempo surpasses 2024’s whole by Q3, the obvious steadiness belies important underlying market shifts.

– Dynamics as soon as thought-about momentary—similar to unlabeled funding rounds and extremely uneven fundraising timelines—have solidified into everlasting options of the market, forcing corporations and traders to make each choice depend.

I. Capital Focus and Blurring Benchmarks

Mega Offers Dictate the Digital Well being Market Map

Mega offers (rounds of $100M+) have been the defining drive of 2025. Nineteen such financings have closed this yr, already surpassing the full-year 2024 depend. These outsized rounds—together with investments in Attempt Well being ($550M), Judi Well being ($400M), and Inspiren ($100M)—account for 39% of whole funding. This focus funnels {dollars} right into a slender set of corporations and reinforces the dominance of mega funds, with practically 80% of mega offers this yr having a mega fund on the time period sheet.

The Normalization of Unlabeled Raises

What began as a market stopgap has change into routine: 35% of 2025’s financings stay unlabeled. Whereas unlabeled rounds supply startups a practical option to prolong runway and delay valuation haircuts, they weaken conventional benchmarks and create a “noisier pipeline” that’s tougher for enterprises to evaluate for readiness and long-term partnership potential.

The Thinning Sequence B Pipeline

The fundraising velocity development is very uneven. Whereas the median time between most funding rounds (e.g., Seed to A) fell in 2025, the time between Sequence A and Sequence B considerably lengthened to a median of 27 months, up from 17 months within the 2023 cohort. Coupled with a thinning deal move (simply 30 Sequence B raises by Q3 2025, down from over 60 yearly in prior years), this alerts that the trail to changing early traction into scalable development has change into far much less direct.

II. The Workflow Race: Startups Go Horizontal, Incumbents Double Down

Exercise is overwhelmingly clustered round workflows and infrastructure, which now supply the clearest path to differentiation. Scientific workflow and non-clinical workflow are 2025’s two most-funded worth propositions, capturing a $1.3B lead over the remainder of the sector.

Startups Push for Horizontal Breadth

Rock Well being studies that digital well being startups are utilizing funding, partnerships, and M&A to construct horizontal breadth and evolve from level options into complete platforms. M&A deal quantity is up 37% from final yr, with 166 acquisitions logged to date.

- Examples: Judi Well being acquired care navigator Amino Well being to push into affected person navigation, and the acquisition of EHR and workflow belongings now represents the biggest share of 2025 offers (16%).

- Differentiation: To face out, startups are publishing ROI knowledge, forming joint ventures with well being methods, and tailoring their fashions for particular specialties, signaling traction earlier than incumbents reset the baseline.

Incumbents Reset the Baseline in Digital Well being Market

Incumbent EHR distributors are quickly integrating once-differentiating startup workflows into their core methods, accelerating the market reset.

- Epic is folding clinician help (Artwork), income cycle automation (Penny), and patient-facing AI (Emmie) into its EHR.

- Oracle is following go well with with an AI-enabled affected person portal and income cycle suite.

- Innovaccer is launching Gravity, an AI-first conductor designed to route fashions and knowledge throughout a typical platform.

Click on here to view Rock Well being’s Q3 2025 Digital Well being Funding report.

{kind=link}